For many Indian families, a significant portion of monthly income is committed to loan repayments even before other household expenses are considered.

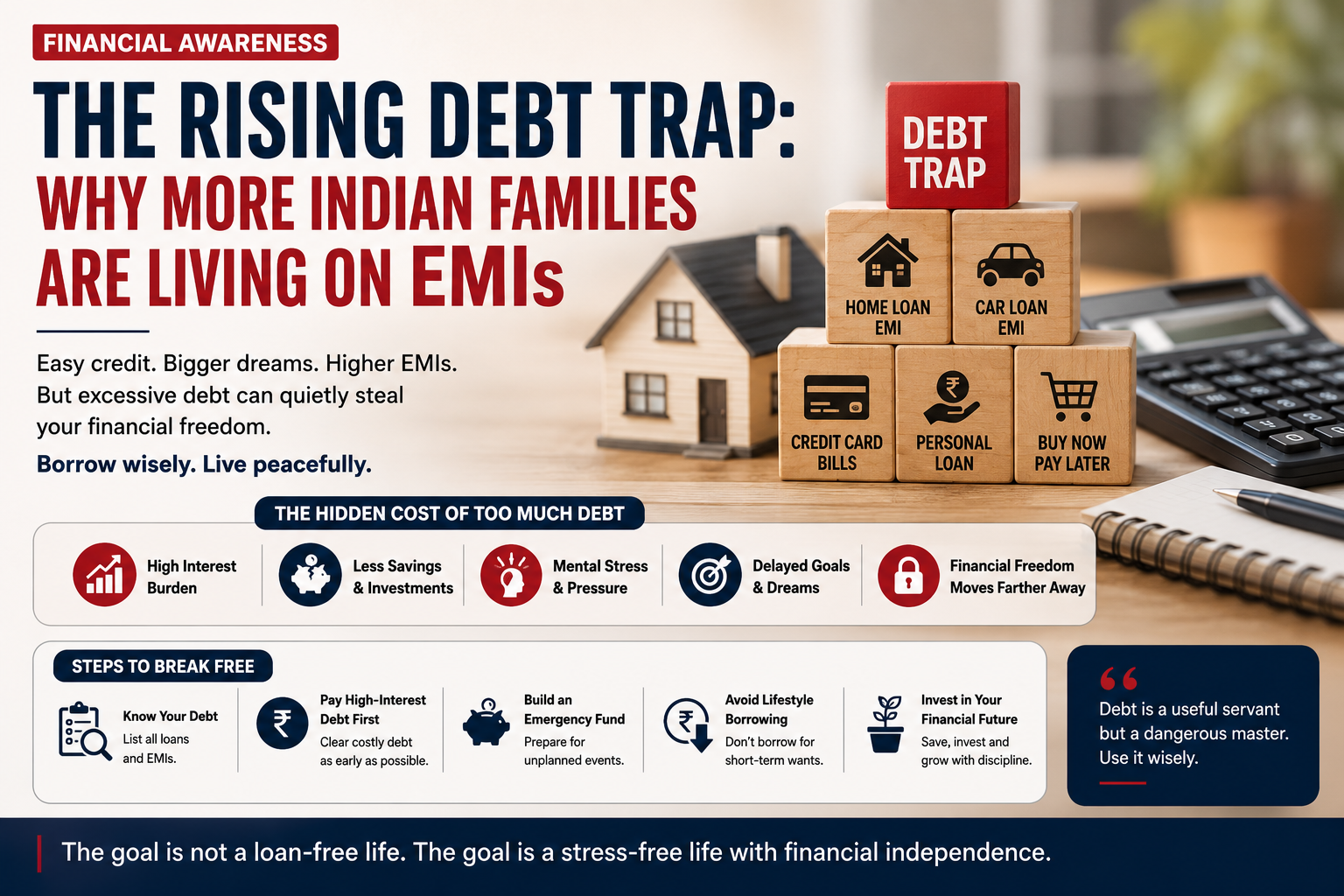

Home loans, vehicle loans, personal loans, credit card dues, and consumer financing schemes have become increasingly common components of household budgets. What was once viewed primarily as a financial convenience is now a regular part of life for many households.

As access to credit expands, an important question emerges: how much of a family’s future income is already allocated to repayment obligations?

Growing Dependence on Credit

Over the past decade, access to credit has become easier through banks, non-banking financial companies, and digital lending platforms.

Personal loans, credit cards, consumer durable financing, and “Buy Now, Pay Later” options are now widely available. While these financial tools can help individuals manage expenses and achieve important goals, excessive reliance on borrowing may create long-term financial pressure.

Financial experts often note that borrowing can be beneficial when used prudently, but repayment commitments must be carefully assessed before taking on new debt.

Factors Contributing to Higher Debt Levels

Lifestyle Expansion

As incomes rise, spending patterns often change. Many households choose to upgrade homes, vehicles, electronic devices, and lifestyle-related purchases. In some cases, these purchases are financed through loans or credit facilities.

Easy Access to Financing

Advances in technology have simplified the borrowing process. Loans that previously required extensive paperwork can now be approved digitally within a short period. While convenience has improved, repayment obligations remain in place for months or years.

Limited Emergency Savings

Unexpected expenses such as medical emergencies, job loss, business disruptions, or urgent household needs may lead families to rely on credit if adequate savings are not available.

Understanding the Cost of EMIs

Monthly instalments often appear manageable when viewed individually. However, the overall financial impact may include:

- Interest payments over the loan tenure

- Reduced capacity for savings and investments

- Financial stress during income disruptions

- Delays in achieving long-term financial goals

- Limited flexibility during emergencies

Financial planners frequently advise households to evaluate total repayment costs rather than focusing solely on monthly EMI amounts.

Productive and Non-Productive Debt

Not all borrowing has the same financial impact.

Loans used to acquire long-term assets, such as housing, may contribute to wealth creation over time. On the other hand, borrowing for short-term consumption or rapidly depreciating items may require more careful consideration.

A useful question for borrowers is whether the debt contributes to a long-term objective or primarily supports immediate consumption.

Steps Toward Better Financial Management

Families seeking greater financial stability may consider several practical measures:

Review Existing Debt

Preparing a list of all outstanding loans and monthly repayment obligations can help households understand their financial position.

Address High-Interest Debt

Credit card balances and unsecured personal loans often carry higher interest rates and may warrant priority attention.

Build an Emergency Fund

Maintaining a financial cushion can help reduce dependence on borrowing during unexpected situations.

Evaluate New Borrowing Carefully

Assessing affordability and long-term repayment commitments before taking on additional debt can support better financial decision-making.

Financial Stability and Income Control

Financial stability is influenced not only by income levels but also by the extent of financial obligations attached to that income. Managing debt responsibly can improve a family’s ability to save, invest, and prepare for future needs.

Credit remains an important financial tool when used carefully and within one’s repayment capacity. However, maintaining a balance between borrowing, saving, and spending is essential for long-term financial well-being.

Rather than focusing solely on consumption, many financial experts encourage households to prioritize sustainable financial planning, emergency preparedness, and wealth creation over time.

About the Author

Vaasu Challa is a Financial Journalist and Public Interest Writer who writes on financial literacy, household finance, and consumer awareness. His work focuses on helping individuals and families make informed financial decisions through practical and accessible financial education.